First Quarter

|

FRED Data:

Inflation: 1.8% Unemployment: 3.9% Net Exports: -494 Billion GDP Growth: -4.8% |

|

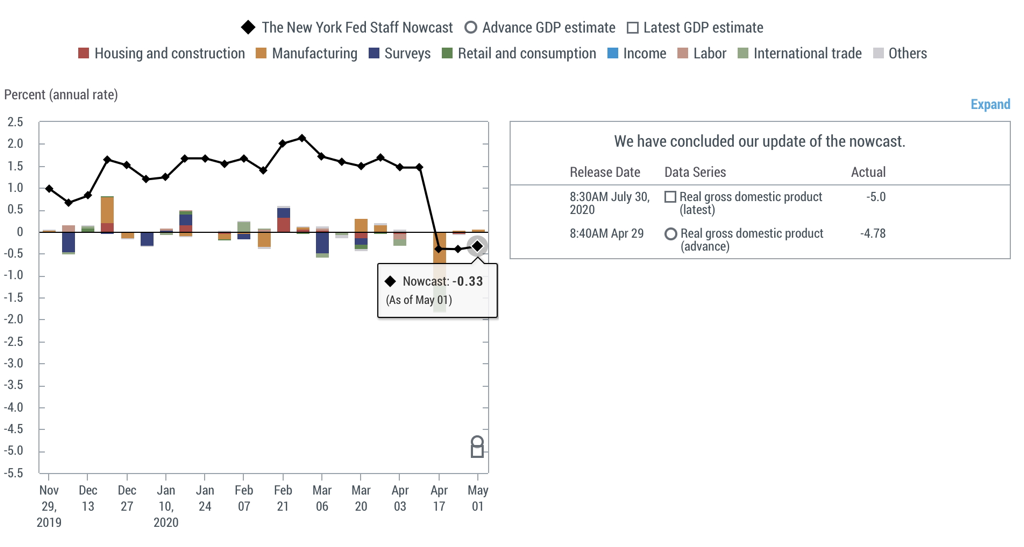

Prior to the lockdown in March, the first quarter of 2020 was seen as the apex of a decade-long growth since the 2008 financial crisis. In February, we saw the lowest unemployment rate in US history (3.6%), stable inflation, and significant job growths. Unfortunately, the self-induced pandemic resulted in a significant number of furloughs that eventually turned into terminations. As a result, unemployment increased the slightest bit, signaling the massive amount of layoffs to come. Of course, shutting down the economy lead to a dip in production, and thus a 4.8% hit to GDP. At this junction, the only policies available to the federal government are transfer payments (stimulus checks, unemployment checks, etc.) to assist the general public.

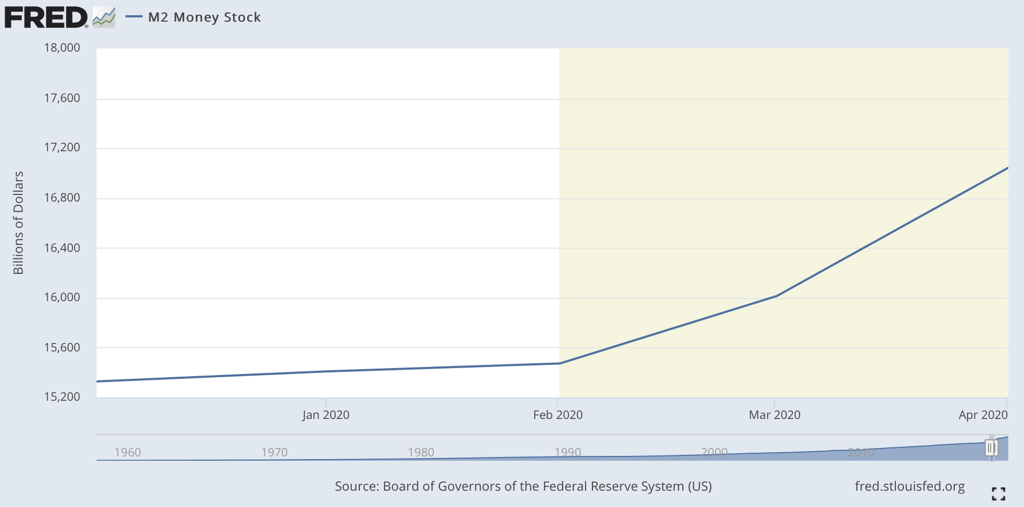

Naturally, to fend off the storm to come, the government issued more debt in the form of treasury bonds. To assist in the economic crisis, the Federal Reserve began to launch quantitative easing (QE) to purchase up some of the t-bonds issued by the government. Launching QE sharply raised the money supply (as seen in the graph above) and created fears of future inflation.

Second Quarter

|

FRED Data:

Inflation: 1.0% Unemployment: 13.32% Net Exports: -545 Billion GDP Growth: -31.4% |

|

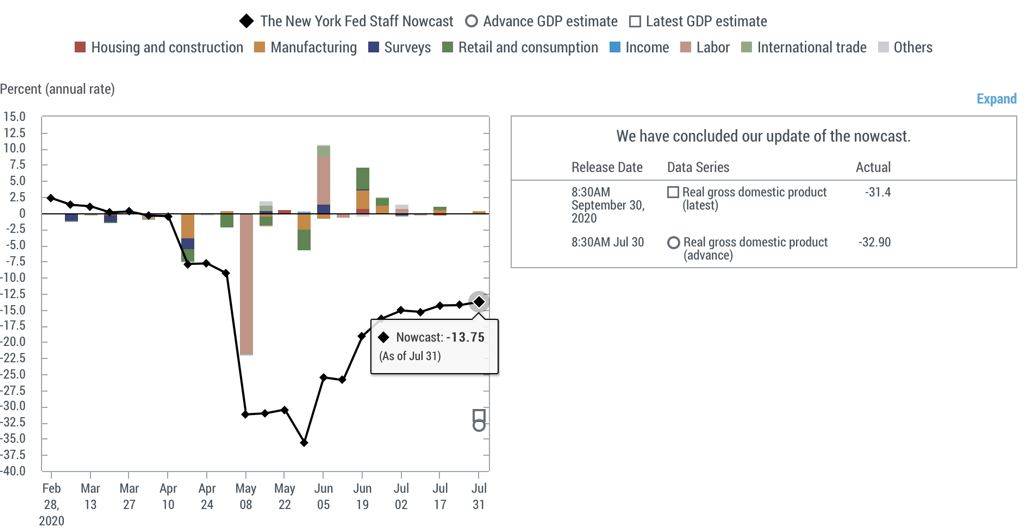

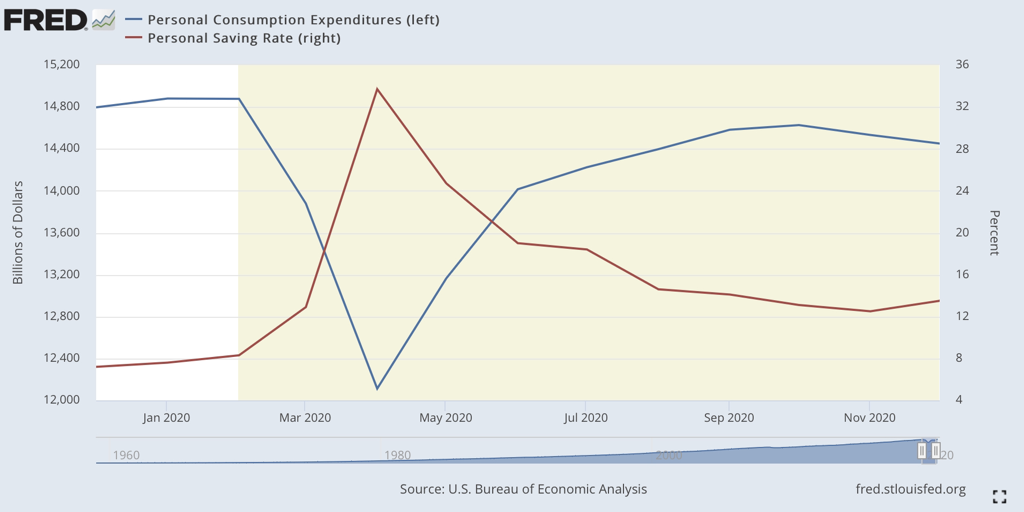

In raw numbers, the second quarter was probably the most devastating. Here the reality of the pandemic set in— more workers were laid off, more businesses shut down, and GDP saw one of its most significant downturns in US history (the second quarter of negative growth officially rendering the US in recession). As explained by the Phillips curve, higher unemployment meant lower inflation: lower streams of income reduces demand for goods which puts a downward pressure on prices.

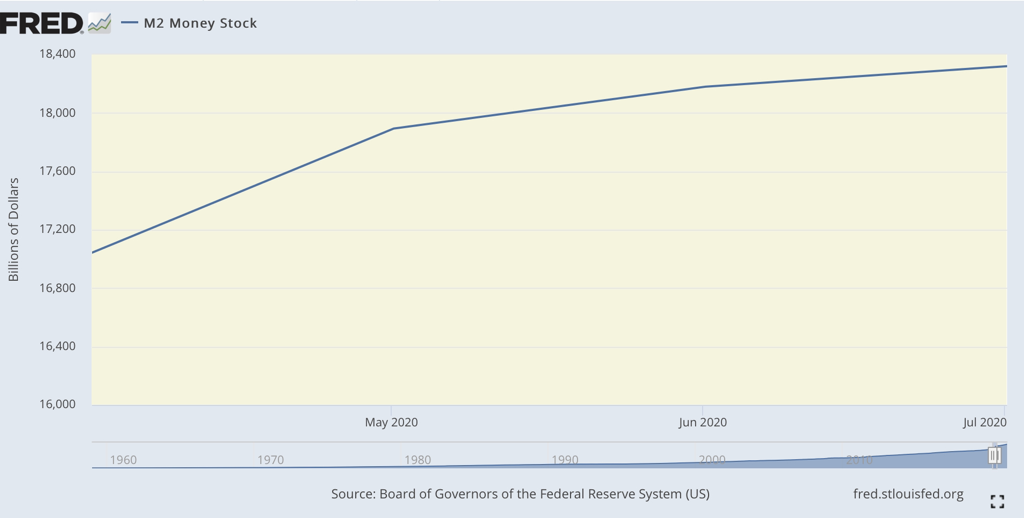

Because of this deflationary pressure, in the short term many economists were unbothered by the increase in money supply since the velocity of money had decreased significantly. However, in many cases, deflation can be more detrimental than inflation. In the face of inflationary pressure, the Fed has the option of increasing interest rates to reduce the velocity of money. But to fend off the recession, the Fed had already lowered interest rates. Should deflation become hyperdeflation, there would be very little avenues to combat it. That being said, there wasn’t much worry about this. Since the recession was self induced, consumer spending would see a significant spike should the lockdown policies reverse.

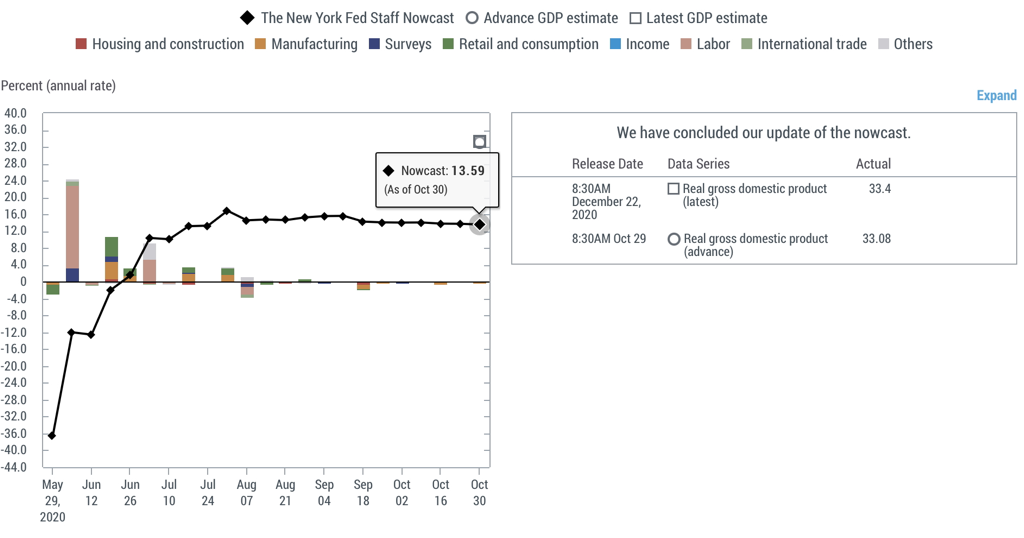

Third Quarter

|

FRED Data:

Inflation: 1.4% Unemployment: 8.80% Net Exports: -736 Billion GDP Growth: 33.4% |

|

As the businesses adapted to the new normal, they developed new business models that allowed them to employ more workers or bring back those on furlough. However, this positive growth in GDP was only possible because of the significant decline in the previous quarter. While many businesses were able to sustain themselves with new models, others were restricted by policies on what facilities were considered “essential” by the government. When combined with the general decline in consumer demand from the recession, many businesses were closing down for the foreseeable future. Thus the economy was recovering in a counterintuitive way, while the short term losses in employment were reversed, the maximum capacity of potential employment was slowly declining.

In the second quarter of 2020, the consumers not only decreased spending due to the decline in personal income, but also because there was a general sentiment to save during the recession. Such a decline in consumption translated into less revenue for businesses struggling during the pandemic. Thus many small businesses were put out of business.

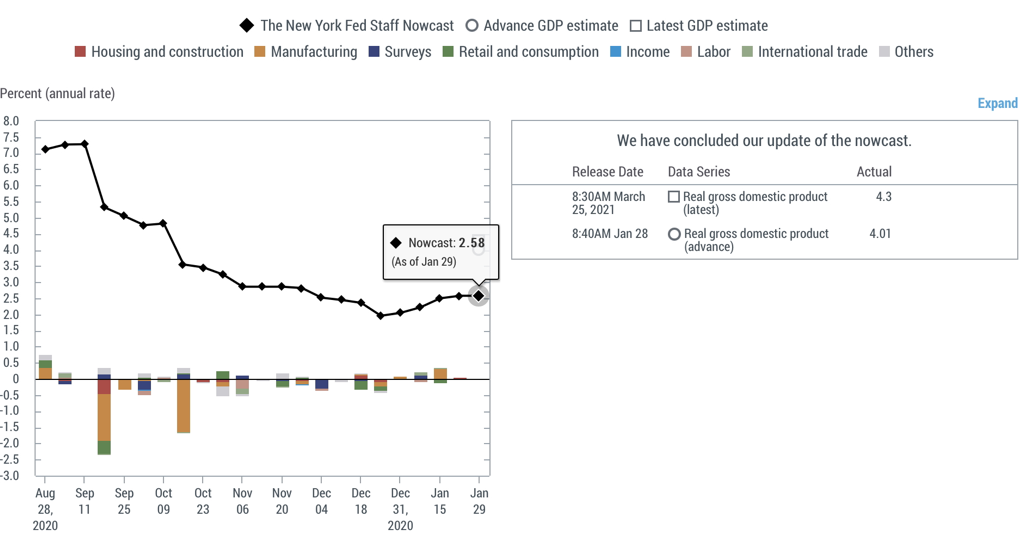

Fourth Quarter

|

FRED Data:

Inflation: 1.4 % Unemployment: 6.79% Net Exports: -804 Billion GDP Growth: 4.3% |

|

The fourth quarter saw continual growth and significant decreases in unemployment. Some restrictions began to lift and the path to recovery seemed open.

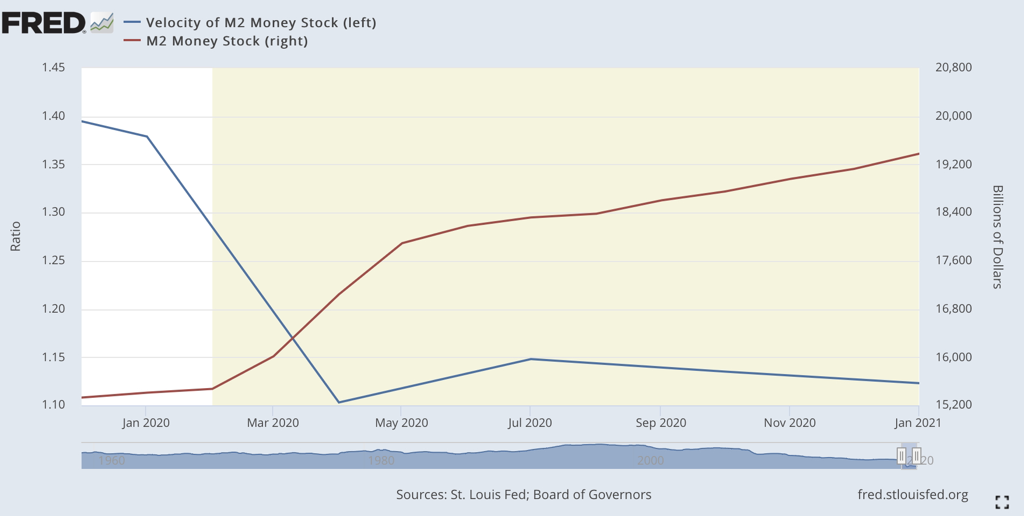

As you can see in the graph above, in the year 2020 the velocity of money and the money supply had an inverse relationship. Theoretically speaking, this should keep inflation at lower levels (which during that time it did). However, should the velocity of money reverse its direction without the money supply seeing a significant reduction, the US would see a noticeable amount of inflation. At this point, the Fed hoped for higher levels of inflation so that the average rate of inflation throughout the year would be around 2%. This idea of average inflation worried many economists who had little faith in the Fed’s ability to accurately manipulate inflation rates. The impact of this decision will be interesting to see in 2021.