First Quarter

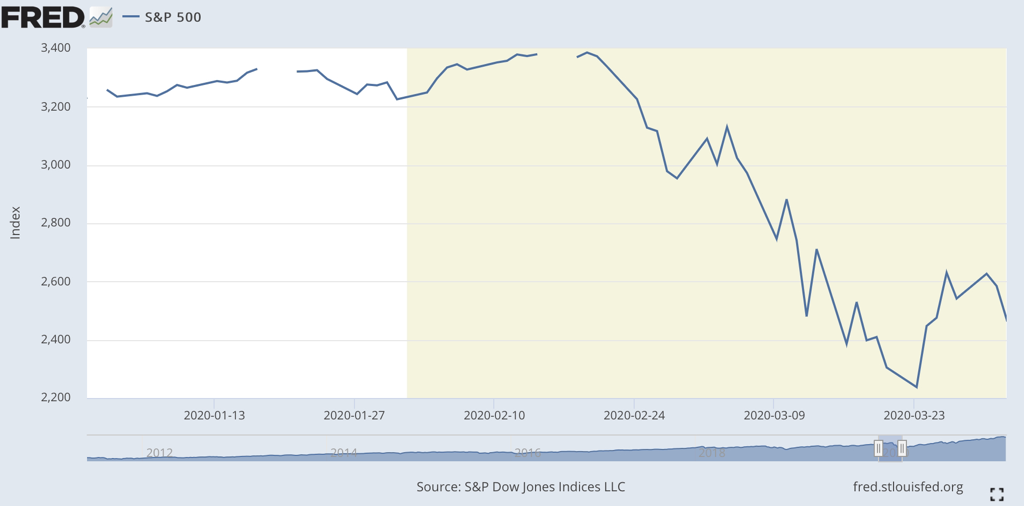

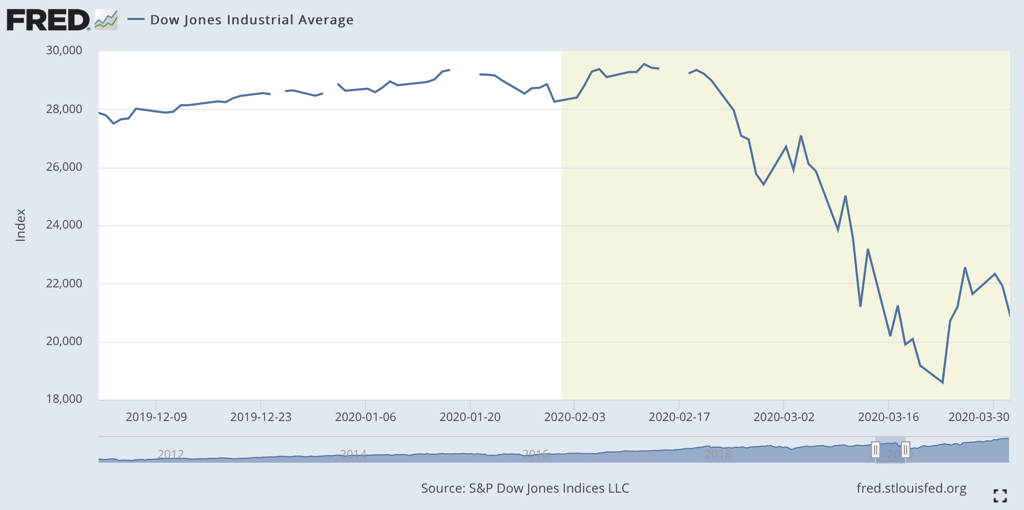

Stock MarketAfter a record highs on all fronts, US stock markets saw a ridiculous decline from news on a potential lockdown due to the global pandemic. Such a sharp decline was instantly compared to Black Monday in 1929, and the popular perception was that a similar pattern of slow market recovery will be the future of stock markets.

|

S&P 500

Dow Jones Industrial Average

Wilshire 5000

|

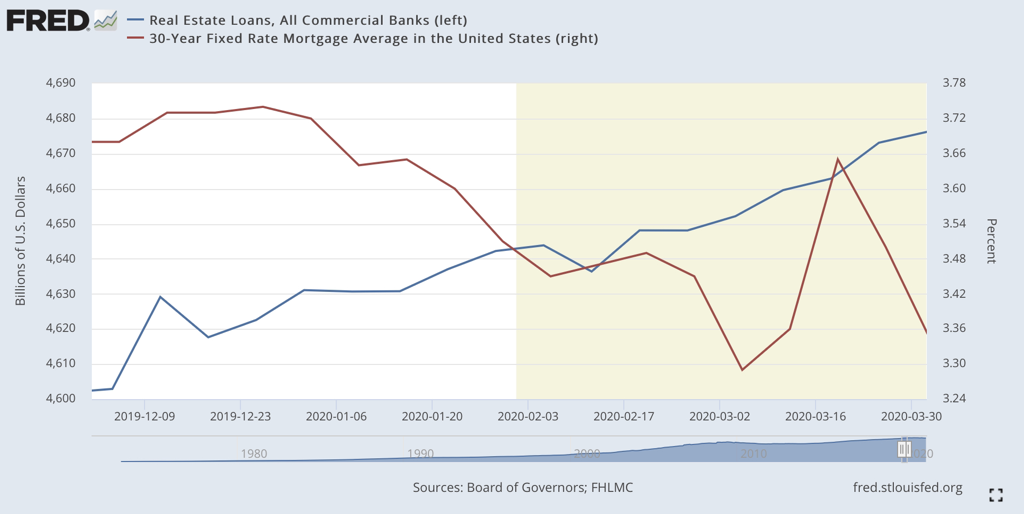

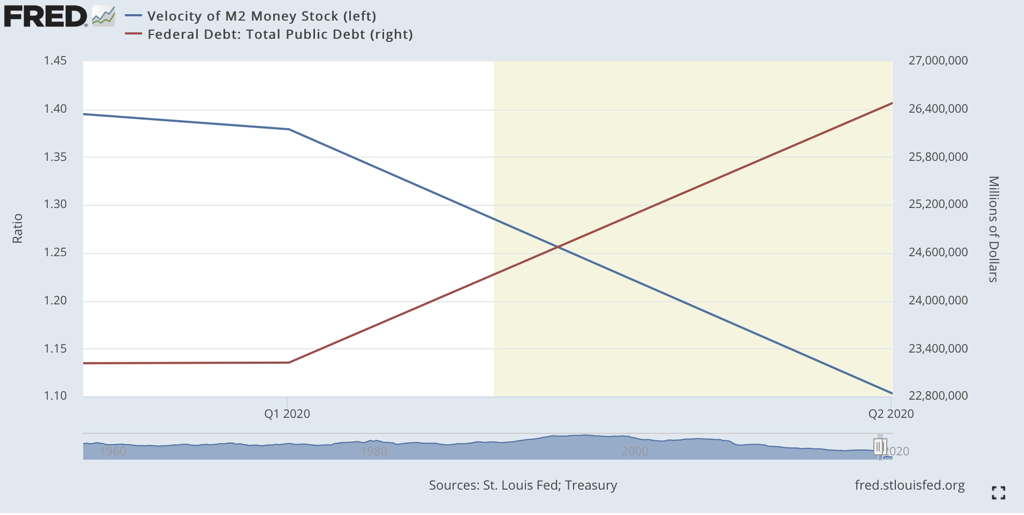

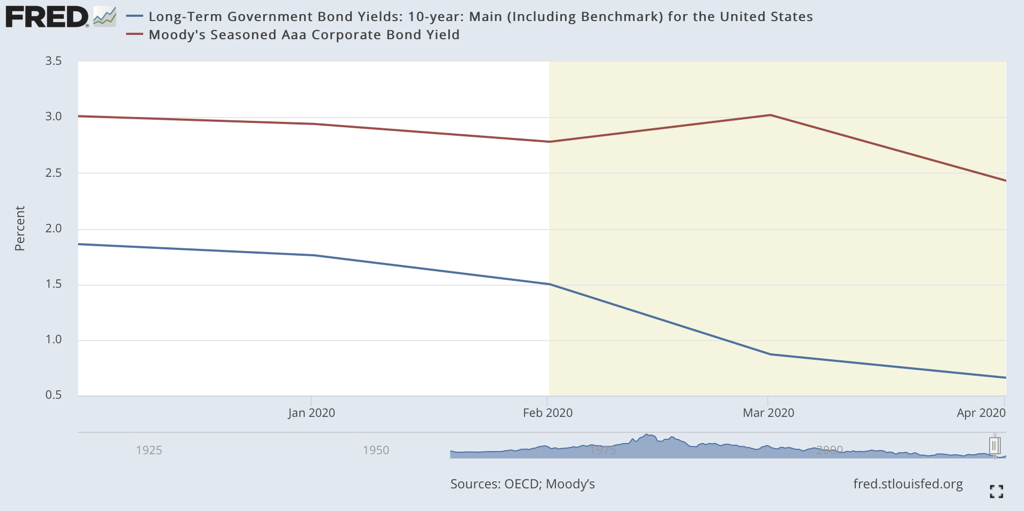

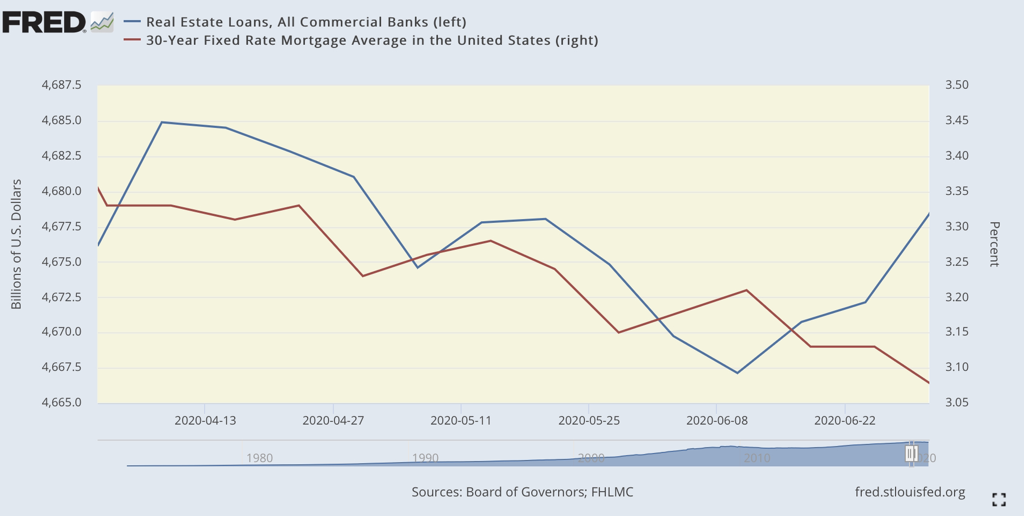

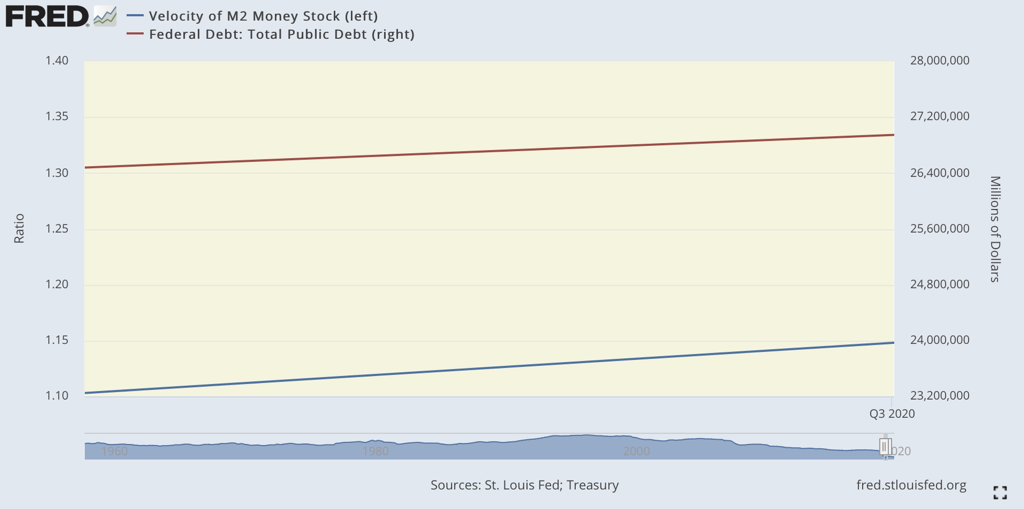

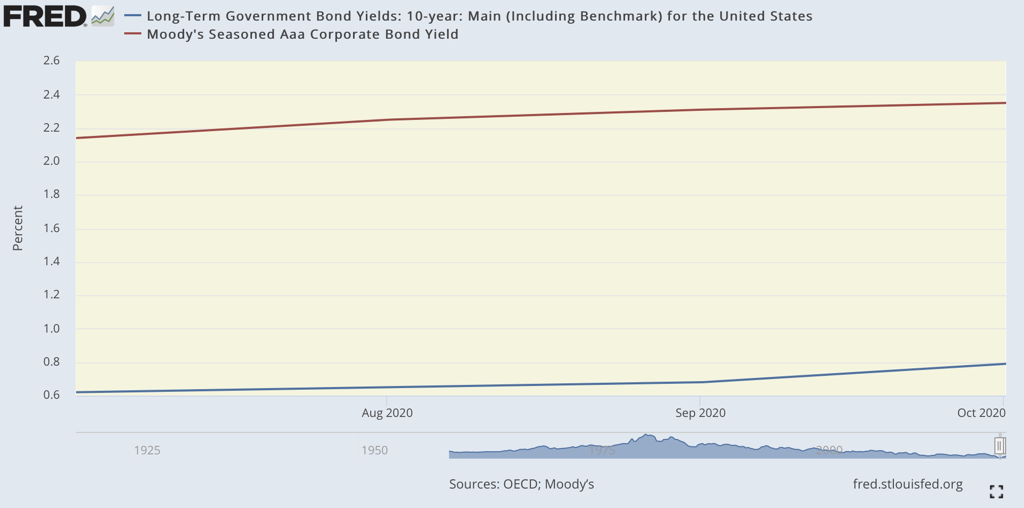

Lending StandardsThe relationship between the velocity of money and bank loans are the determiners of inflation during a period in which the money supply increases drastically. Due to the fractional banking system, deposits are multiplied to the inverse of a bank’s reserve requirement and thus increase the amount of money perceived to be in the economy. However, should banks tighten their lending standards, the velocity of money will see a decline. Looking at the graph that compares the velocity of money to federal debt, you can see that quarter one showed little change from Q4 of 2019. However, as the pandemic progressed in the second quarter, lending standards tightened at the sight of uncertainty as US federal debt shot way up to battle the pandemic. Looking at the housing market, you can see the moment in which uncertainty in the first quarter was at its peak. Around the same time the stock market saw its decline, interest rates on 30-year mortgages shot way up.

|

Housing Market

Velocity of Money

Bond Yields

|

Second Quarter

Stock MarketThe second quarter saw a surprising rebound in stock markets. Initially, many economists and investors, believed that this growth would be a dead cat bounce, similar to the short period of growth that followed 1929’s Black Monday. In theory, the initial decline would cause investors to repurchase securities at cheaper prices, but, as the recession continued and companies yielded unfavorable quarterly profits, short term investors would sell those assets and continue to drive down the price.

|

S&P 500

Dow Jones Industrial Average

Wilshire 5000

|

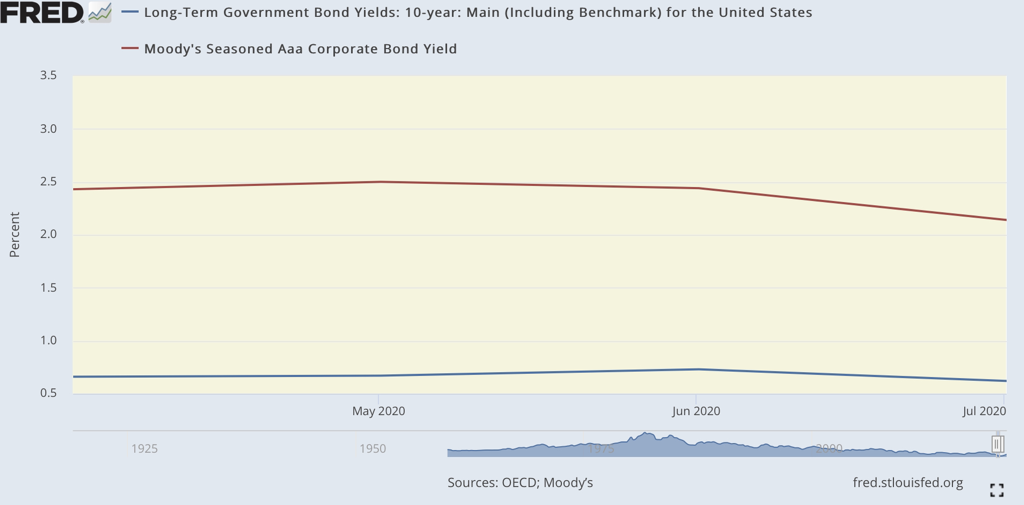

Lending StandardsHere we see something interesting. As the Fed goes full swing into expansionary monetary policy, bond yields and mortgage interest rates decline together with the amount of money loaned to the general public. Yet, despite that the velocity of money increases in the second quarter. Now a possible reason for this increase might be the influx of stimulus checks in April. Though people were more inclined to save, a trillion dollar influx of money should raise the velocity of money from its already declined state.

|

Housing Market

Velocity of Money

Bond Yields

|

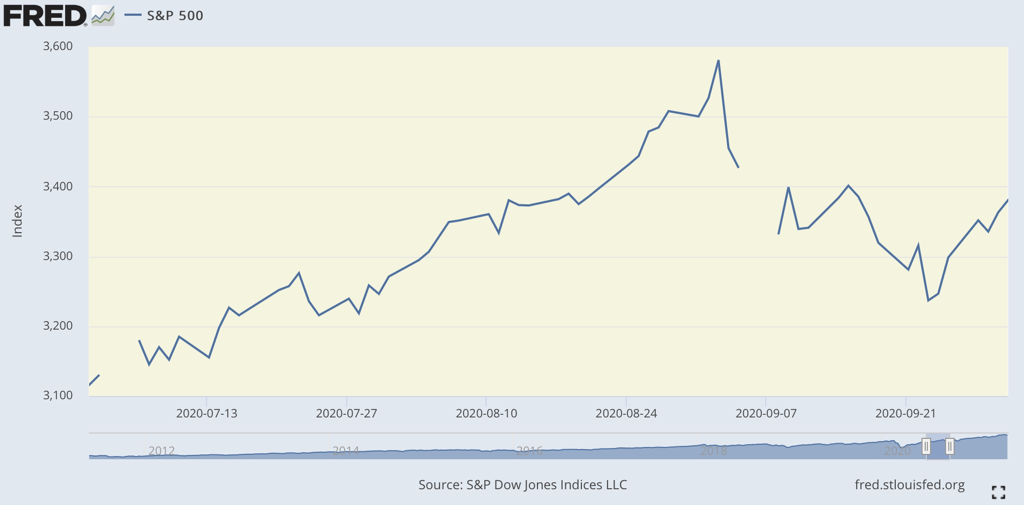

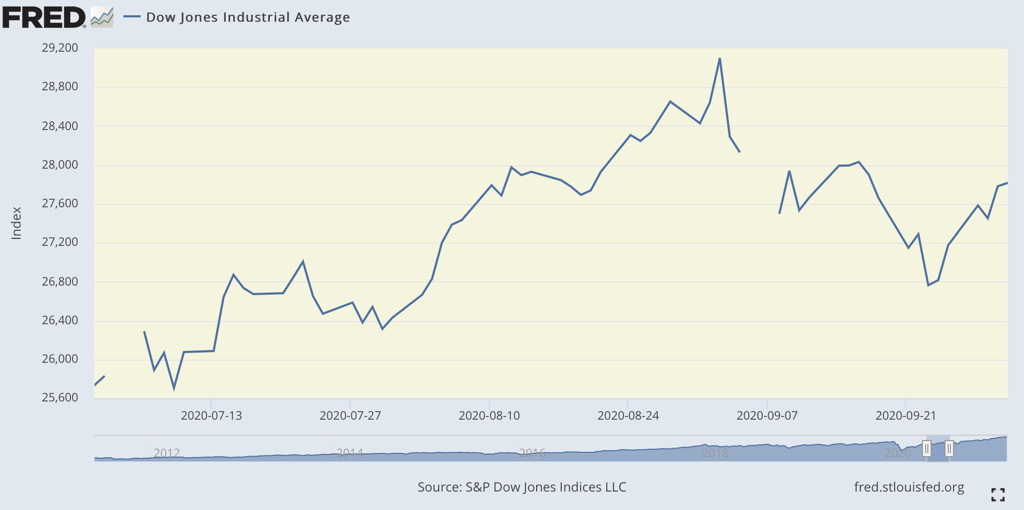

Third Quarter

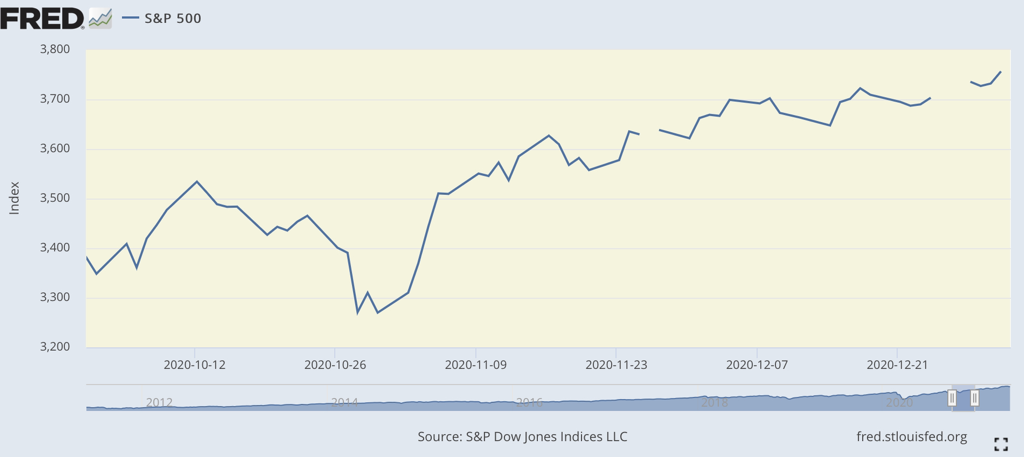

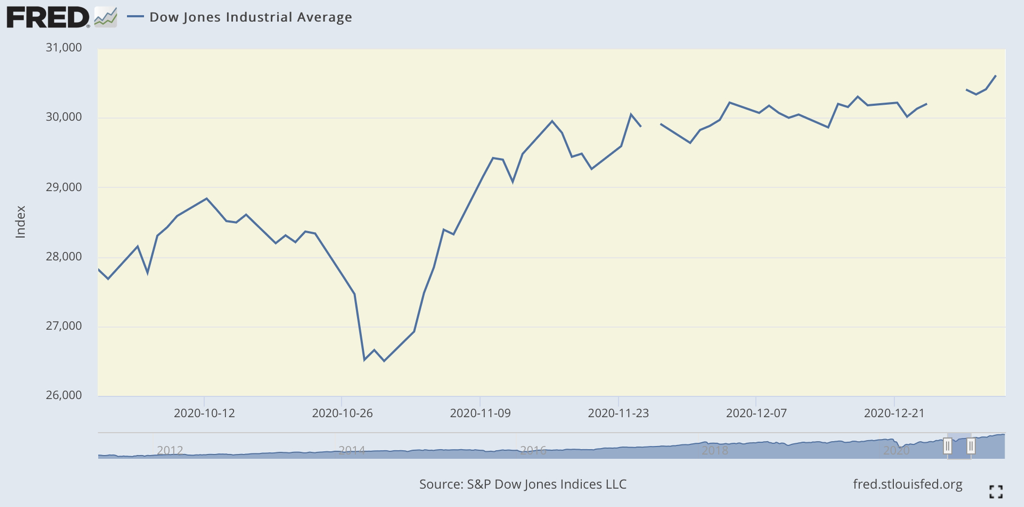

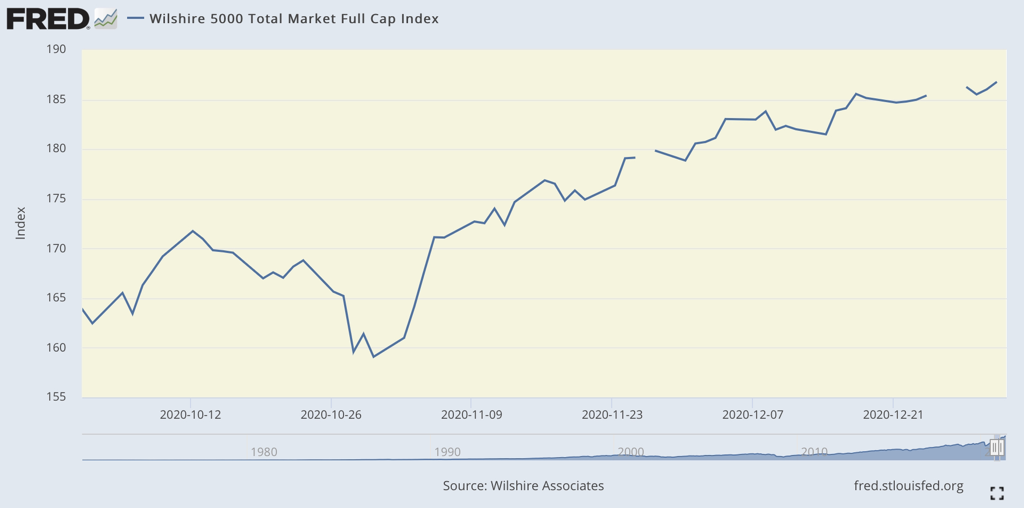

Stock MarketAgainst the expectations of many, stock prices continued to rise and soon new record highs were achieved. Such a dichotomy between mainstreet and wallstreet was baffling. Many theories were formed on the matter— the most popular of which was that there simply was nowhere else for people to put in their money. Unlike the 1929 crash, in which savings and bank solvency were crushed by bank runs, there were multiple factors in place that would prevent the worsening of this financial crisis. For one, living in a primarily digital system made citizens inclined to leave their deposits in banks, allowing banks to maintain their solvency. Additionally, the “self-induced” nature of the pandemic reduced panic among the masses. Rather than viewing the stock market as an untrustworthy and unreliable means of earning money, the common man became more inclined to try their hand in investment. Trading apps like Robinhood and WeBull grew in popularity and more capital was poured into the stock market. Of course, this effect was compounded once stimulus checks arrived in the mail. For institutional investors there simply was no where else for them to put their capital. So naturally, they too poured money into the stock market, adding to the bullish pressure on prices.

|

S&P 500

Dow Jones Industrial Average

Wilshire 5000

|

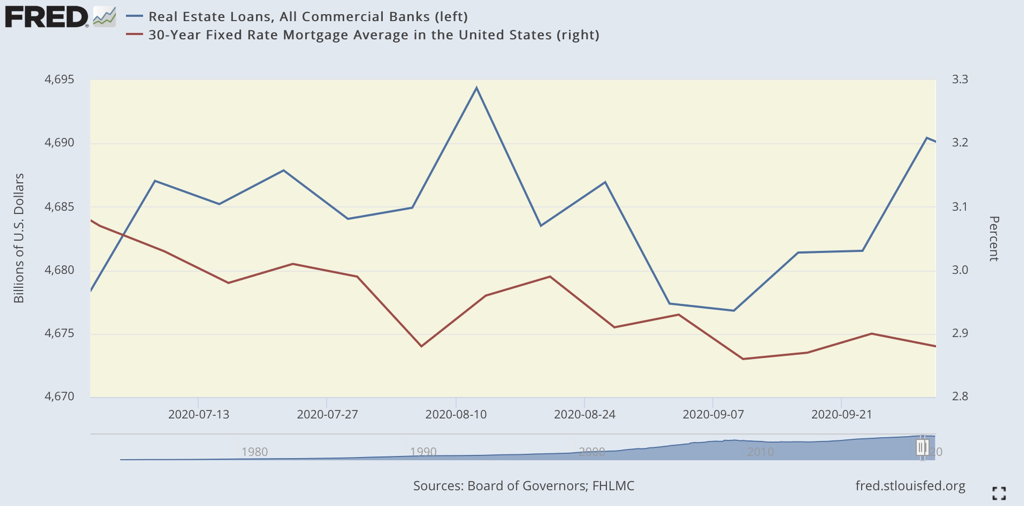

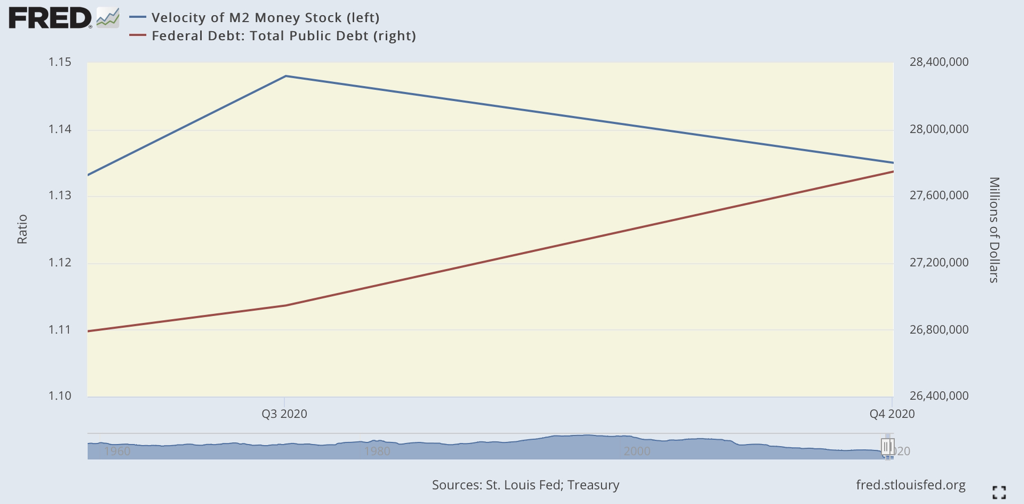

Lending StandardsAfter the influx of stimulus checks passes, the velocity of money declines yet again. Bond yields remain stable, and, oddly enough, there’s quite a bit of volatility in the amount of money loaned by commercial banks.

|

Housing Market

Velocity of Money

Bond Yields

|

Fourth Quarter

Stock MarketThe fourth quarter was also marked by record market highs. Another theory for the unreasonable increase of stock prices was that investors had adapted to and capitalized on the expansion of QE by the Fed. When the Fed launches QE, they purchase t-bonds and a few mortgage-backed securities. As a result of the increase in demand, there is downward pressure on t-bond interest rates. Since the US t-bond is used as a baseline rate for all corporate bonds, a downward pressure on its interest rates trickled down to the rest of the bond market. In response to this, more investors were inclined to pour more of their money into a booming stock market in hopes for better returns.

|

S&P 500

Dow Jones Industrial Average

Wilshire 5000

|

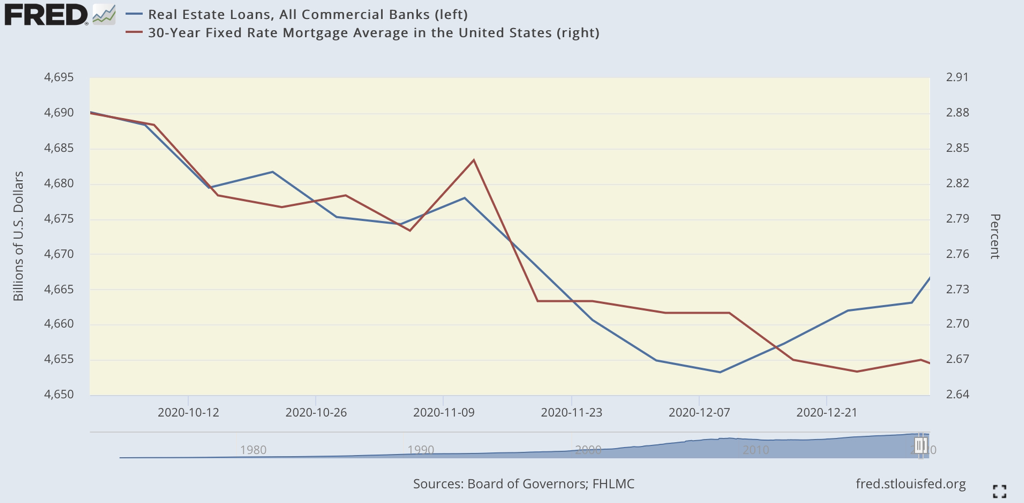

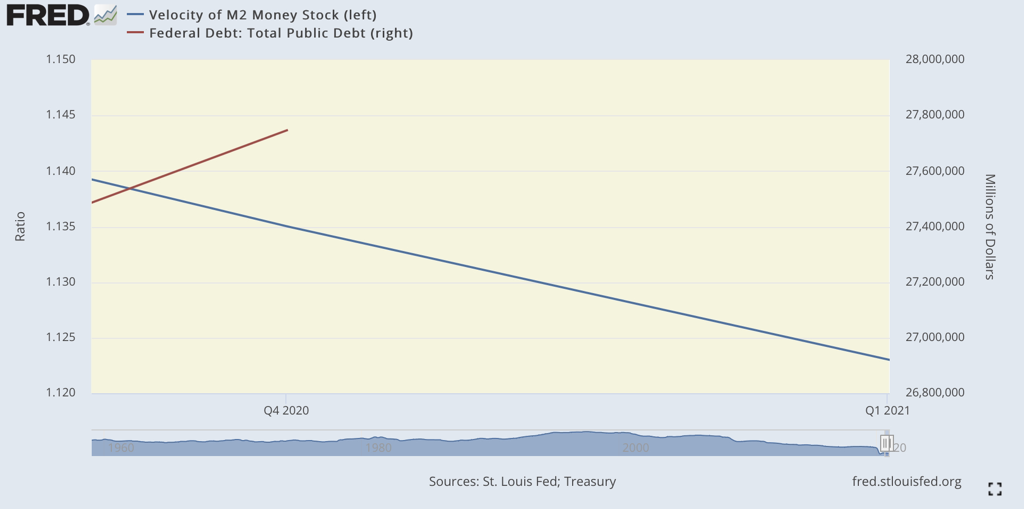

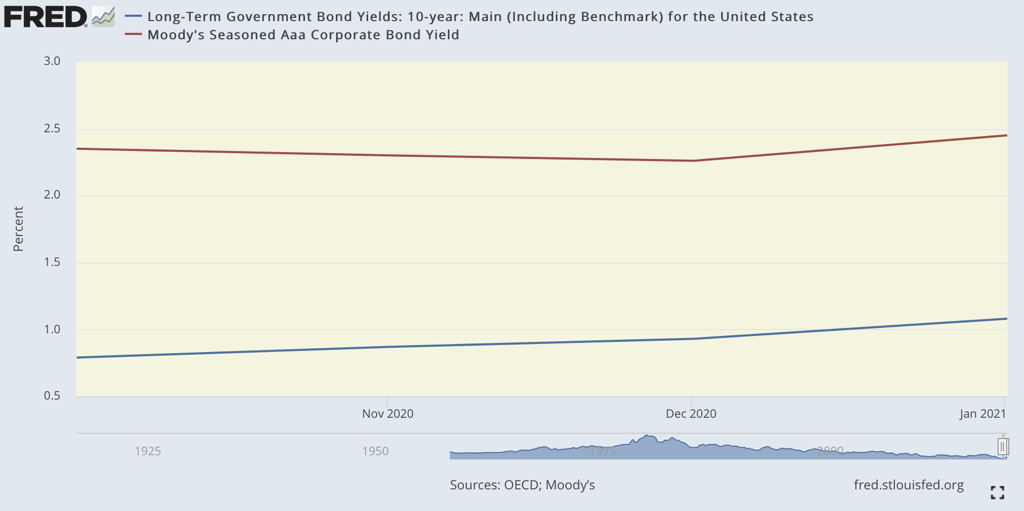

Lending StandardsThough a more prominent recovery should be underway, both the velocity of money and the amount loaned by commercial banks see a sharp decline. For some reason, banks continue to be tight-fisted on lending. Without significant lending, the recovery from the pandemic is less dramatic. However, a lower velocity of money limits the amount of inflation that could be caused by the explosive increase in M2. In the transitional period between the pandemic normal and the post-pandemic normal, the Fed’s ability to reduce M2 in conjunction with commercial banks’ increase in loans (i.e. and increase in velocity) will be the primary the determinant of inflation moving forward.

|

Housing Market

Velocity of Money

Bond Yields

|